Sick of overdraft fees? Me too. Learning how to avoid overdraft fees is a skill that everyone needs.

At some point, we’ve all experienced a bank overdraft fee. They’re terrible.

When you get the notification, it’s like hitting a wall. It’s the same as pulling the Go to jail card in a game of Monopoly. You can almost hear your bank telling you to “Stop. Go directly to jail; do not pass go, do not collect $200”. Except in this case, you’re likely hearing that your account is negative and that you now owe the bank $35 in money that you don’t have.

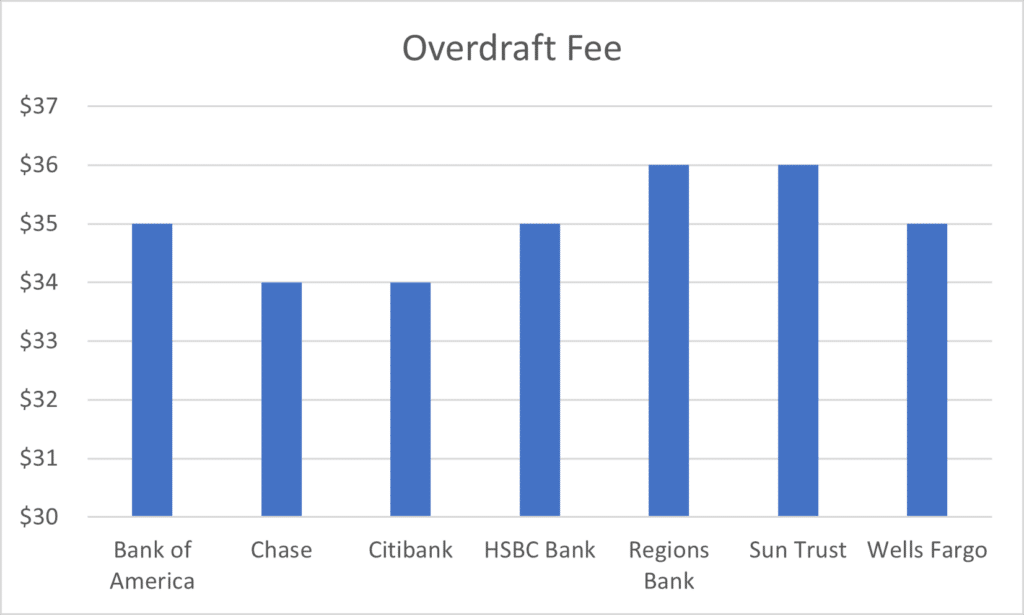

Yeah, overdraft fees are expensive and annoying. We’re talking an average of $35 depending on your bank.

Data from https://www.nerdwallet.com/article/banking/overdraft-fees-what-banks-charge

The best way to avoid overdraft fees is by avoiding overdrawing your account in general. The good news is that there’s a lot of different ways you could go about that.

Avoid overdraft fees by keeping your checkbook balanced, paying for everything in cash, looking into alternative options, or linking your bank accounts.

Below we’ll be talking about the pros and cons of each of these solutions.

Balance your check book and keep a buffer

This is probably the best recommendation on this list. It’s always a good idea to have an emergency fund. Most experts recommend having an emergency fund of at least $400.

You never know when you might have an emergency expense or an unexpected bill. It could be a doctor bill, car repair, or even something else. Regardless, it’s always good to have at least a little bit of a financial cushion.

It’s important to know how to build a budget properly. Some people prefer using budget planners to help them stay on track.

The plus with budgeting is that you’ll stay financially independent. You won’t have to ask for money, or even fight with the bank to get a refund for the overdraft fee. Best of all, it will help instill good savings habits that can help protect you from other fees down the road as well.

Budgeting is a valuable tool that can help you better manage your money. It can help with paying off debt and saving for retirement. There’s nothing wrong if your goal to avoid overdraft fees is the catalyst to start budgeting.

The downside to budgeting and keeping a buffer is that it’s not always realistic in a short period of time. It takes time to save up a few hundred dollars. It could easily take a few months at least. Plus, if you find yourself in a situation where you need to spend your emergency savings, you’ll have to start over from scratch again. Saving an emergency fund is one thing. Maintaining it is something different.

Pay for everything with cash

This is another great recommendation on this list as it also provides useful financial skills. Paying with cash is both a way to stick with your budget and a way to help prevent using debt. When you pay for everything with cash, you can follow a tighter budget.

Cash budgets work for a number of reasons. For starters, it pressures you to acknowledge how much you’re spending. Each time you buy something, you’ll see how much cash you use to pay. Secondly, it allows you to have an idea of how much money you have in a spending period. You can see the physical wad of cash you have, and it helps you set expectations for yourself.

The main reason I like this strategy is because it’s a set it and forget it kind of plan. You can determine how much money you want to spend in a week. Some weeks you might want to spend more or less than others. Regardless, you can always check that you’re still saving some money so long as you withdraw less than you make. If you don’t use your card, you won’t have to worry about overdrafting your account.

The downside is that cash budgets aren’t always convenient. There are times you have to use a plastic card. You may need to pay for something online or over the phone. You might forget your envelope of cash at home. There may be a fee if you don’t use your card at all within a month. The worst downside is if you lose your envelope, you won’t have any money until your next payday.

Look into alternative options with lower fees

There are other strategies I like more, but I still felt I should include this one in the list. This was a life hack I found when I was younger and really struggling with overdraft fees.

It’s no secret that overdraft fees are expensive. On average, they’re $35. That’s the price of a really nice dinner. These types of fees do nothing to help you cover the purchase you’re making in the moment. One alternative would be a personal loan. The average personal loan runs about $20 for every $100 borrowed. It can be pricey, but it costs less than an overdraft fee.

If you’re not familiar with personal loans, there are a lot of options out there. Find which type is best for your needs.

The good news is that you’ll spend less than you would with an overdraft fee, and you’ll still be able to cover the purchase you were trying to make. If you’re worried about your credit score, you can relax. Most personal loan providers won’t run a credit check. Their service is to just help you buy what you need and spread out the purchase cost over two pay periods.

The downside is that there’s still a fee in all of this. This plan doesn’t help you get out scot-free. Although you’ll manage to save money, you won’t manage to get out of the situation without paying something.

Switch up your bank and link your accounts

Maybe a lack of money isn’t the issue. Maybe the issue is that you often forget to transfer money over to your checking account.

Some people just get busy and forget to move money to their account until it’s too late.

If you have two separate accounts with the same bank, you can link them together. This is helpful for those moments when you know you have the money, you just don’t know how much is in your checking account.

Simply link your bank accounts. That way, if you overdraw in one, it can automatically transfer money from the other account to cover the difference.

On the upside, this is a great plan if you have a hefty savings or retirement account. It provides enough of a buffer that you can go about your spending worry-free.

The downside is that not everyone has multiple bank accounts with the same bank. They may just have one bank account or may have accounts with different banks. So, if you have accounts with multiple banks, it might be time to consolidate them. Or at least two of them.

Switch your bank account over so that you have two accounts with the same bank. Some banks allow their service for free. Others may charge a fee when you use the automation feature, even if they’re two internal accounts. However, the cost will likely be a fraction of an overdraft fee.

You can avoid an overdraft fee

It’s important to learn how to avoid overdraft fees.

Overdraft fees do nothing to benefit you. They just sit as a reminder that you don’t have as much money in your account as you need.

Worst of all, they’re not proportional to the amount you overdraw. The fee is usually about $35 regardless of if you accidentally overdraft your account by $1 or $100.

If anything, overdraft fees hurt you at a time that you’re already down. No one wants to be reminded that their bank account is empty.

It’s 2021, and we’re done with arguing with our bank over overdraft fees. Instead, we’re learning to avoid the issue entirely. Hopefully these four tips help you avoid future overdraft fees.